Most industries experience consolidation - there are few exceptions and the office products and supplies industry is certainly not one of them. In this blog, the fourth in a multi-part series, I'm going to explore some scenarios for the reseller's merger endgame and the impact this may have on the future of the aftermarket for office products and supplies and on the independent resellers.

The Aftermarket, Office Supplies and a Major Tipping Point (Part I) - The Tipping Point

The Aftermarket, Office Supplies and a Major Tipping Point (Part II) - The OEM Endgame

There are three segments of the office products industry to assess when examining the mergers endgame;

1. The OEM's (Examined in Part II)

2. The Aftermarket Manufacturers (Examined in Part III)

3. The Resellers (The Subject of this Part IV)

The Resellers

There are many resellers of office products and supplies. At first sight, most observers would automatically assume it's a very competitive, and diversified reselling environment.

In fact, by our estimate, there are well over 5,000 reseller's in the United States alone. However, on a closer look, and as demonstrated in the chart below, 83% of the estimated $25B in U.S. ink and toner retail sales are conducted by less than 2% of the total number of resellers.

For the purposes of developing an understanding of the reseller's potential mergers endgame, there are two events of particular interest to us. Firstly, the busted Staples, Office Depot acquisition and, secondly, (very much related) the definition of the market as may be determined by government authorities, for the purposes of deciding whether or not a proposed acquisition should be allowed. Having an understanding of these will help to better understand what may happen in the future.

There have been many studies surrounding the characteristics of industries over time but, it's generally accepted that in most industries, there will be consolidation and that market concentration will develop. In order to measure how concentrated an industry is, two calculations are widely used by Fair Trade Authorities, such as the FTC, in determining whether or not proposed acquisitions should be allowed to proceed.

1. The Concentration Ratio (CR) is calculated by adding the percentage share of the largest enterprises in the particular market or industry. Usually, the top three are used (hence the label CR3) so, for example, if the top three companies have a 50% share then the CR3 = 50%.

2. The Herfindahl-Hirschman Index (HHI) is calculated by squaring the market share of all competitors and summing the total. For example, if the leading enterprise has a market share of 25% then 25 x 25 = 625, if the next largest player has a share of 15%, then 15 x 15 = 225, a running total of 850, and so on until all market participants are accounted for.

The highest value for the index would be if there was a pure monopoly - i.e. one enterprise with 100% market share or 100 x 100 = 10,000. The opposite end of the scale would be pure competition, for example, 10,000 competitors each with one, one-hundredth of one-percent market share - i.e. (.01 x .01) = 0.0001 x 10,000 = 1.

With that brief foundation now let's take a look at the resellers in the office products and supplies space.

There are four scenarios shown in the following four tables. Scenario One and Three explain a pre-merger and post-merger market for Office Products and Supplies while Scenario Two and Four explain a pre-merger and post-merger market just for Office Supplies (ink and toner only).

Scenario 1 - Let's look at this concept from the perspective of the United States market for all office products and supplies (estimated at an $85 billion annual market) with regards to the shares held by the various resellers in the various reselling channels.

| Channel | Count | Total Sales ($M) | Share % | HHI |

| Tier-1 Reseller Big-Box | 9 | $67,450 | 66.7% | 946 |

| Tier-1 Dealer | 100 | $7,364 | 16.2% | 4 |

| Tier-1 Reseller (Internet) | 4 | $6,625 | 8.9% | 31 |

| Tier-1 Reseller | 2 | $1,900 | 4.2% | 12 |

| Tier-2 Dealer | 500 | $1,090 | 2.4% | 0 |

| Tier-3 Dealer | 5,000 | $750 | 1.6% | 0 |

| Grand Total | 5,615 | $85,179 | 100% | 993 |

Scenario 2 - Now let's look at the same concept with a narrower definition of the market - i.e. the United States resellers market for ink and toner (excluding all other office products) and widely estimated as a $25 billion annual retail market.

| Channel | Count | Total Sales ($M) | Share % | HHI |

| Tier-1 Reseller Big-Box | 9 | $16,674 | 79.2% | 1,311 |

| Tier-1 Dealer | 100 | $4,050 | 8.6% | 1 |

| Tier-1 Reseller (Internet) | 4 | $2,219 | 7.8% | 20 |

| Tier-1 Reseller | 2 | $1,045 | 2.2% | 3 |

| Tier-2 Dealer | 500 | $599 | 1.3% | 0 |

| Tier-3 Dealer | 5,000 | $412 | 0.9% | 0 |

| Grand Total | 5,615 | $25,000 | 100% | 1,355 |

Look at how much difference there is between Table 1 and Table 2 with regards to the two key measurements, market share concentration and the HHI index! Simply by narrowing the definition of the market from all office products to just that of the market for ink and toner, we can see the largest sales channel controls nearly 80% of ink and toner sales, with an overall HHI of 1,355.

By definition, the FTC would define the overall office products market as "not concentrated" (HHI = less than 1,000) but the market for ink and toner as "moderately concentrated" (HHI is between 1,000 and 1,799).

Scenario 3 - Now let's look at the same two scenarios already summarized in Table 1 and Table 2, but assume that Staples had successfully acquired Office Depot.

| Channel | Count | Total Sales ($M) | Share % | HHI |

| Tier-1 Reseller Big-Box | 8 | $67,450 | 66.7% | 1,631 |

| Tier-1 Dealer | 100 | $7,364 | 16.2% | 4 |

| Tier-1 Reseller (Internet) | 4 | $6,625 | 8.9% | 31 |

| Tier-1 Reseller | 2 | $1,900 | 4.2% | 12 |

| Tier-2 Dealer | 500 | $1,090 | 2.4% | 0 |

| Tier-3 Dealer | 5,000 | $750 | 1.6% | 0 |

| Grand Total | 5,615 | $85,179 | 100% | 1,677 |

I've highlighted the cells in Table 1 and 3 that have changed - in Table 1 they're green and in Table 3 they're red.

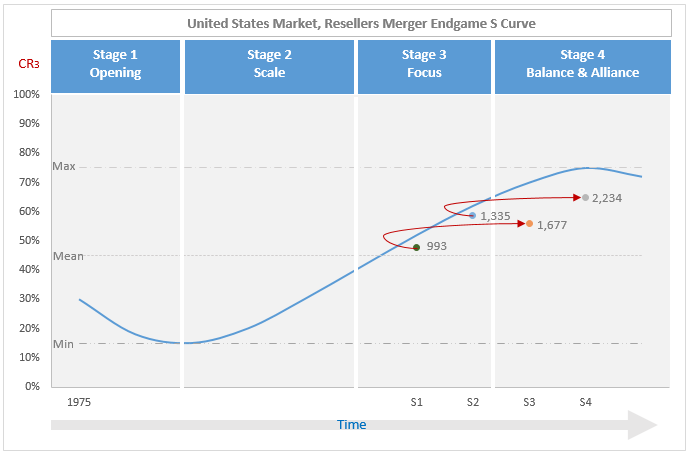

You can see one big-box enterprise is eliminated as Office Depot is merged with Staples. Overall the reseller count drops from nine to eight, the overall HHI score increases from 993 to 1,677. This is still within the FTC boundaries of a "moderately concentrated" industry but, a big increase (684) from the pre-merger index score, and approaching the threshold for being judged as a "highly concentrated" industry.

Scenario 4 - Now let's look at the final Table 4 and compare the more narrowly defined market for ink and toner before and after the planned acquisition of Office Depot by Staples.

| Channel | Count | Total Sales ($M) | Share % | HHI |

| Tier-1 Reseller Big-Box | 8 | $16,674 | 79.2% | 2,234 |

| Tier-1 Dealer | 100 | $4,050 | 8.6% | 1 |

| Tier-1 Reseller (Internet) | 4 | $2,219 | 7.8% | 20 |

| Tier-1 Reseller | 2 | $1,045 | 2.2% | 3 |

| Tier-2 Dealer | 500 | $599 | 1.3% | 0 |

| Tier-3 Dealer | 5,000 | $412 | 0.9% | 0 |

| Grand Total | 5,615 | $25,000 | 100% | 2,234 |

Once again I've highlighted the cells that changed. In Table 2 they're green and Table 4 they're red. You can see one big-box enterprise has been eliminated as Office Depot is merged with Staples and the reseller count drops from nine to eight. The HHI score increases from 1,355 to 2,234 and the defined market now becomes a "highly concentrated" industry with a substantial increase of 879 index points resulting from the proposed acquisition event.

Had the FTC used the market for ink and toner for assessing whether or not Staples should have been permitted to proceed with their acquisition of Office Depot, then I don't think the outcome would have been any different, as their objections would most likely have been similar. As it was, the FTC used the market for office products (excluding ink and toner) and further narrowed the market to argue that the Staples / Depot merged entity would have had monopolistic power in the B2B contract stationary sector. Staples failed to provide a counter argument to the FTC's position and ultimately withdrew from the deal.

The four scenarios I've explained above are plotted on the Industry Consolidation Curve shown below. This helps demonstrate the concept of what the FTC was concerned about with regards to Staples proposed acquisition of Office Depot and the progression toward increased market concentration and reduced competition.

The Big Box Retailers - Staples and Office Depot

Staples made it clear during the 15-month failed acquisition process that they feared the increasing threat posed by Amazon, while also claiming there was significant competition from all the other traditional office products and supplies resellers. While competition from resellers such as CDW, Insight, Walmart, Target, Costco, Sam's, and even the OEM's is unarguable, the Court accepted the FTC's argument that the threat from Amazon in the B2B contract stationary market was in the future, not the present, and was, therefore irrelevant to the proceedings.

The B2B contract stationary business conducted by Staples and Office Depot are the "crown jewels" of these two big-box resellers.

-

As we know, neither Staples nor Depot can shrink their "brick and mortar" retail footprint fast enough to accommodate consumers changed buying habits. Walk-in retail is threatened by changing consumer purchasing habits, not specifically by Amazon.

-

Both Staples and Office Depot have their own powerful e-commerce platforms to compete with Amazon.

-

We know Amazon has a renewed focus on its Business Services initiative, relaunched back in April 2015, and it is this threat that probably keeps the Staples and Depot executives awake at night.

However, while this may become a significant threat in the future, the difficulty for Amazon is their expertise is more geared to B2C than B2B and a B2C solution is not what B2B customers are generally looking for.

There's a high level of integration between Staples / Depot and their B2B customers that Amazon cannot currently match. At least for now Amazon will most likely continue to find it quite difficult to win substantial portions of this B2B business.

When looking at the financial indicators for Staples and Office Depot, it's clear that Office Depot is the weaker of the two entities. However, they're hardly in a distressed situation, announcing better than expected earnings in November 2016 and the sell-off of their European and other overseas operations. This indicates they are gearing up for a focused U.S. strategy and increasingly cost-efficient operations.

As a result of its failed acquisition, Staples had to pay Depot a $250 million break-up fee. While both Depot and Staples, at time of writing, are trading at close to book value, Depot has informed its shareholders it's authorized to spend up to 100% of that breakup fee buying back its own shares.

-

If the leadership at Depot doesn't believe in its future then they wouldn't be likely to be spending this windfall on a buy-back of their shares.

-

Depot is able to continue to finance closing their traditional twenty-five thousand square foot stores out of cash-flow.

-

The target count for the traditional store footprint is down to 1,200 or so by the end of 2018. This represents a reduction of over 40% from the peak at the time of the 2013 merger with OfficeMax.

-

Depot is accelerating the opening of their "stores of the future" with 120 or so of these 5,000 square-foot, "local neighborhood" style stores, planned by the end of 2017.

I find it quite difficult to project what may come next in this sector of the reseller market. We know there's not going to be a combination of the two big guys, from which the most synergies could be extracted, and from which a more powerful enterprise could probably be created. We know both Staples and Depot have positive cash flow and strong balance sheets while Depot, at least, believes its shares are under-valued. Neither enterprise is distressed, or likely to be going out of business so, where may they be going?

Some possibilities:

-

Amazon acquires either Staples or Office Depot

-

A Chinese investment group acquires either Staples or Office Depot

-

U.S. Private Equity acquires either Staples or Office Depot

-

Staples continues to acquire the best Tier 1 dealers

-

Depot continues to wring-out synergies from OfficeMax acquisition

-

Otherwise continue as-is

Longer-term, I do think both Staples and Depot face significant challenges and, of the potential scenarios listed above, I think for now, a combination of options four, five and six are the most likely. Potential acquirers will sit on the sidelines while the market continues to mature.

What about the other two channels?

The Independent Resellers

The outlook here may be more predictable. It's interesting that Office Depot still considers a brick and mortar presence to be important for local markets, as indicated by way of their plans for opening 120+ of their new "stores of the future" retail concept. These plans indicate that Office Depot believes there's still a need for a physical presence in local markets. This implies there may also be an opportunity for independent resellers leveraging their local footprints, so long as they develop capabilities to match the service and performance standards of Depot and Staples. However, regardless of whether or not the independent resellers can effectively compete with Staples and Depot in their local markets, I expect a significant thinning of the ranks. The strongest Tier-2's will acquire the best of the Tier-3's and will then, subsequently be acquired by the strongest Tier-1 players. Many of the weakest Tier-3 will simply go out of business.

The Internet Resellers

What most people may think of in terms of e-commerce and the future, may not be the way it plays out, at least not in the short and medium term. As we know, Amazon is the powerhouse of e-commerce even though Staples and Office Depot also have strong e-commerce portals.

It's clear Amazon wants to break into the B2B office products channel and, we know, from Staple's efforts to convince the FTC to allow their acquisition of Office Depot, that they (Staple's) fear the threat of Amazon in this B2B space. Fortunately, at least in the short term, for Staples and Depot, it appears the Amazon B2C platform is not suitable to meet the needs of the typical B2B customer they currently serve. However, given Amazon's resources, it may only be a matter of time before they figure out a solution to this problem, and start to win share in this lucrative segment of the market.

Overall, I believe the scope for new entrants in the Internet Reseller Channel, at least in terms of competing with Amazon, eBay, NewEgg, LD Products and even Staples and Office Depot, is very limited.

It's possible, of course, that we could see some consolidation with Staples, Depot or even NewEgg perhaps acquiring LD Products. However, I don't see significant changes taking place with the current leaders that make up the Internet Reseller Channel, apart from the relentless advance of Amazon and the possible entry of Alibaba. However, Alibaba is a whole different story and I'll try and tackle that at a later time.

In the next post in this series, I'll be summarizing the mergers endgame before moving on to our perspective on the Consumer Adoption Curve and the likely opportunity for aftermarket office supplies in terms of improved market share. When viewed in conjunction with the mergers and acquisitions and the Chinese money, then it becomes much clearer in terms of understanding why it's likely there's to be a significant shift in market shares.

In the meantime, why not check out our free eBook with a comprehensive assessment of the office products industry and the opportunities to develop significant sales growth in a challenging environment despite the ongoing consolidation of a mature industry.