In a mature

In the legacy "push" economy, manufacturers had enough power to push the configurations they favored on their customers but, in a "pull" economy, consumers have the power to pull the products and services configured the way they want. Manufacturers and resellers that recognize this change, and who provide their customers and prospects with a framework to conduct business that allows the resources they offer to be quickly and easily configured to serve a wide variety of needs, will thrive while those who don't will not.

In the legacy "push" economy, manufacturers had enough power to push the configurations they favored on their customers but, in a "pull" economy, consumers have the power to pull the products and services configured the way they want. Manufacturers and resellers that recognize this change, and who provide their customers and prospects with a framework to conduct business that allows the resources they offer to be quickly and easily configured to serve a wide variety of needs, will thrive while those who don't will not.

Players that recognize this fundamental shift in control and who understand the opportunities emerging out of a "pull" economy will thrive, even in a mature, shrinking market.

Unfortunately, adapting to the pull economy requires making changes to legacy business practices. However, change introduces risk, and risk instills a fear of failure. It is this fear that underlies the tendency to cling to outdated business models and to ignore powerful signals indicating the need for change. Sticking to the past means being left behind and being left behind results in an inferior value proposition, fewer new customers, reduced profitability, and increased customer churn. Combining all these negative business trends with a shrinking market turns into a downward spiral with one (usually bad) outcome.

The Distribution Channels

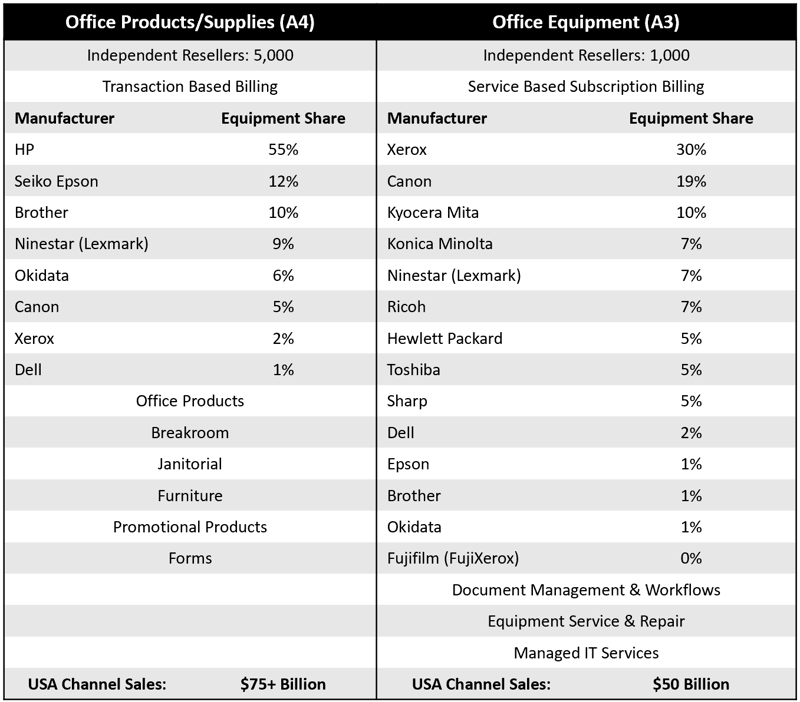

For decades there has been a clear delineation between the office products (A4) and equipment (A3) channels. This delineation exists despite the selling structure being similar in both channels in terms of the value chain sequence that takes place between manufacturers, wholesalers/distributors, and the independent resellers (dealers) who generally serve the end customers. However, what is significantly different is that sales in the office product channel are generally transactional, while sales in the office equipment channel typically take place via monthly service charges.

Note: Equipment market shares and channel size are estimates based on general market knowledge,

Office Products & Supplies

The equipment manufacturers listed in the table make up a significant portion of total sales with their printers and associated supplies. However, these products are surrounded by 50-60,000 other, mostly commoditized, office products such as paper, pens, break-room, and janitorial supplies, plus technology products such as PCs and accessories. For the most part, this vast catalog of products works its way through the distribution channels in a series of transactional sales that culminate with the end consumer.

Transactional sales are vulnerable to competition, and because they're mostly commoditized products, it's relatively easy for customers to switch from one supplier to another to get a better price. Because Amazon is in the office products space, and because Amazon always has the lowest price, more and more consumers, and more and more businesses are switching to Amazon to purchase their office products, their office technology, and their supplies.

Resellers are finding they have to reduce prices to try and fend off this competition. This pricing action reduces the top line as well as profitability, with no end to the downward spiral in sight.

Office Equipment (Print)

Many of the same hardware manufacturers appear in the equipment channel as the office products channel. However, typically, different machines (termed as A3) have been sold into this channel. A3 devices can be defined as the heavy-duty copiers designed for high volume printing, collating, stapling, and other paper handling characteristics with a maximum print size of 11 x 17 versus the maximum 8.5 x 14 (legal) available from the A4 printers more widely sold through the office products channel.

- Unlike A4 equipment, it's much more difficult for a consumer to research the price of new A3 machines independently. Furthermore, not only is it difficult to find out the amount it will cost but getting access to who it can be purchased from is also carefully controlled by the OEM's who assign territories to their authorized resellers.

- The internet has no boundaries which help to explain why you don't see new copier machines listed for sale at reseller's websites. There is no way for the OEMs to control territory boundaries if they were to allow their dealers to post their offerings online.

- Also, unlike the office products channel, most of the sales in the print channel are cloaked under monthly lease payments and so-called "per-click" charges. Resellers charge monthly service fees that are usually inclusive of equipment repair and the supplies needed to operate the equipment.

- Ecosystems have evolved which are designed to facilitate the digitization of documents as documents that used to be printed no longer are which serves to reduce the print volume that underlies the entire business model.

As a result of these factors, it's much more difficult for customers to make cost comparisons between dealers and brands and their respective ecosystems. These circumstances help explain why historically; it has been a much "stickier" sale for the equipment dealer than it has been for the transaction-based business model of the office products dealer. However, even though churn rates have been typically lower, it's now becoming much harder for equipment dealers to ignore the impact of declining print volumes.

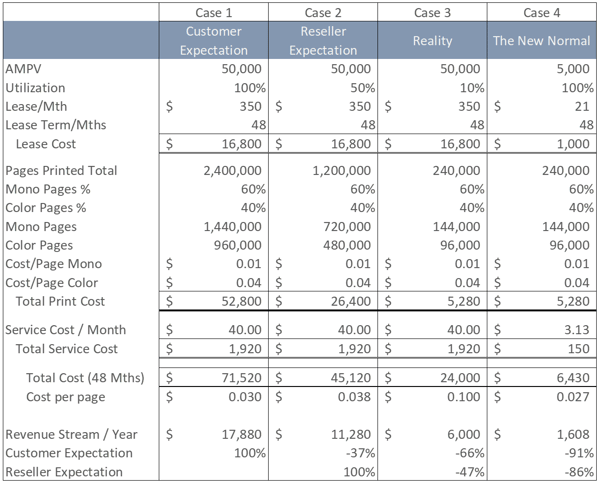

The table, illustrating four different cases, is designed to highlight the problem facing resellers in the print channel. Historically, it has been common practice to roll customers into new leases for replacement equipment. In this example, we're using a $350 per month lease payment on equipment sized for 50K pages per month. Including supplies, in a cost per page model of $0.01 for mono and $0.04 for color, and a $40 per month services contract, the total client cost over four years is $0.03 per printed page or just over $70K at 100% machine utilization.

On the face of it, a blended cost of $0.03 per page is a competitive deal. However, the underlying problem is the actual degree of utilization that's likely to take place on the machine and, to realize $0.03 per page, it requires 100% utilization. What if it's only 10% utilization because the client needs to print 5K pages per month rather than 50K? In these circumstances, the cost per page increases by almost 250% to $0.10 per page.

A more appropriately sized machine (Case 4) may only cost $1K and bring the 4-year expense down to $6.5K at a cost per page of $0.027. Not only is this a 10% per page saving over the original $0.03 benchmark but, more importantly, it's less than a quarter of the annual spend to print the same amount as it costs to generate the print on an under-utilized A3 machine.

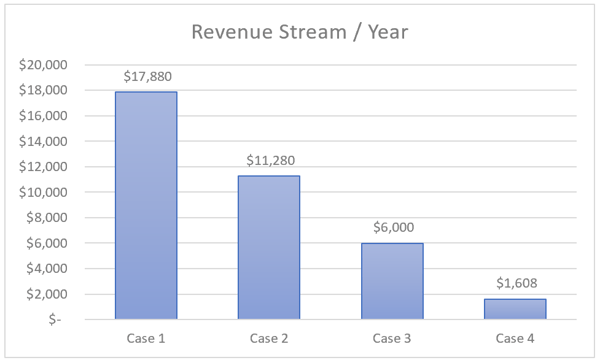

Now think about the problem this creates for the equipment dealer. At 100% utilization on a heavy-duty A3 machine, there's a revenue stream of nearly $18K per year. At 10% utilization, there's a revenue stream of $6K per year, and with a low-cost A4 machine substituted in, there's a revenue stream of $1.6K per year.

While few machines are ever likely (or even intended) to be 100% utilized, let's assume the most realistic expectation by the reseller at the outset of the lease is for an average utilization of 50%. That means the expected revenue from that single placement would be just over $11K per year.

With print volumes declining and utilization at 10% (or 5K pages per month), then the revenue stream drops to $6K per year, or nearly 50% less than the original (most realistic) expectations. Think about this 50% revenue shortfall across an equipment dealers' $10M business.

Now think about the revenue shortfall in the context of an appropriately sized A4 machine purchased for around $1K where the revenue stream falls to $1.6K per year, or 85% less than was expected. Think about this revenue loss in the context of a $10M dealer business.

Now think about this problem (opportunity) from the perspective of a customer with whom the salesman has usually expected to routinely roll a "soon-to-expire" lease into a new one.

Think about how likely it will be for this practice to continue in the context of the 70%+ of buyer's who now choose to do their own research, rather than relying on a salesperson for product information, information that's likely to be slanted toward the specific manufacturer(s) and their ecosystems that they happen to represent. All the customers' have to do is work up a little table, just like we did, and the chances are they'll abandon their "lease-renewal-autopilot-mode" and head toward that $1K printer they've independently learned is a significantly lower-cost solution.

Ultimately, they will either buy the appropriately sized equipment from their current dealer, (who is forced to swallow an 85% decrease in revenue), or they will buy it from someone else.

Of course, most equipment resellers (and legacy channel manufacturers) are becoming increasingly aware of this problem but, because the solution requires facing-up to 50%+ revenue declines, are constrained from doing so.

It has been possible to absorb pressure and delay changes to the business model because all the major players in the "A3" channel have faced the same, common problem. This situation means, without one of them breaking ranks, or a new entrant arriving to disrupt the status quo, the industry has been able to prolong its ability to "push" its over-priced solution to its customers, whether it resulted in them having to pay extra for unwanted capacity or not.

Unfortunately for the legacy players, in prolonging the over-priced solution it is tantamount to having kicked-the-can down the road. While it was possible to maintain this approach in a push economy, it will no longer be sustainable in a pull economy made up of increasingly well-informed buyers eager to transact with providers who allow them to configure products and services according to what they need. So, while the apparent business dilemma may contextualize the reasons why the legacy channel players have resisted change, it doesn't alter the facts, and it's not going to stop the disruption of a tsunami that's now looming over the horizon.

To learn more about the impact of the changing environment on the reseller's value proposition please sign-up for our blog to receive automatic notifications as we publish important new material.

You may also be interested to access to our resource page, "Channel Convergence and the Impact on Independent Resellers" or, to learn more about the full scope of this material and to access in a downloadable e-Book format, please click the cover image below.