The market shares between OEM and aftermarket have been unchanged for many years. In this blog, the sixth in a multi-part series, I'm going to explain about the ink and toner product life cycle and the consumer adoption curve as it relates to aftermarket alternatives. You're going to learn that the stagnation of the aftermarket proposition is mostly related to OEM blocking strategies and not to the lack of consumer acceptance of the aftermarket value proposition.

The Aftermarket, Office Supplies, and a Major Tipping Point Series

The OEM Mergers Endgame (Part II)

The Aftermarket Manufacturer's Mergers Endgame (Part III)

The Reseller's Mergers Endgame (Part IV)

Summary - The Mergers Endgame (Part V)

The Five Steps of the Consumer Adoption Process

- Product Awareness

- Product Interest

- Evaluation

- Trial

- Adoption / Rejection

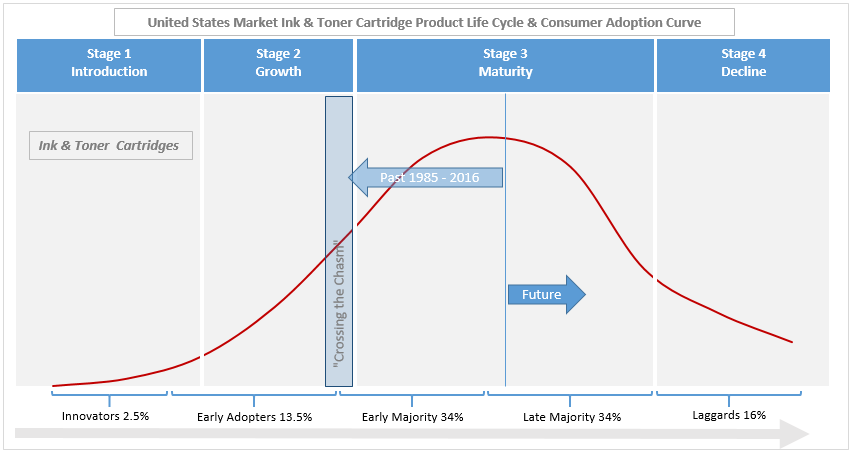

The Five Stages of Consumer Adoption

Consumer adopter distributions follow a bell-shaped curve over time that can be divided into five categories:

-

Innovators (2.5%) - a small group of people eager to try new ideas and take risks

-

Early Adopters (13.5%) - individuals respected by their peers and with a reputation for successful use of new ideas

-

Early Majority (34%) - seldom leaders, take more time to deliberate before willing to adopt a new idea

-

Late Majority (34%) - skeptics only willing to adopt a new idea after the average adopter has already done so

-

Laggards (16%) - traditionalists, the last to adopt an innovation and maybe after it's already obsolete

In terms of office printing and ink and laser supplies, we're in a late-stage, mature industry. Laser printing came on the scene first, back in the mid-1980s and ink arrived a little later, during the early 1990s. The aftermarket remanufacturing industry was born in the mid to late 1980s and the innovator and early adopter consumers quickly propelled the aftermarket remanufactured cartridges to a 20% share by the mid-1990s and 30% by the end of the millennium. With a far smaller share of the color market (less than 10%), aggregate aftermarket share has stagnated around 20% ever since!

In terms of office printing and ink and laser supplies, we're in a late-stage, mature industry. Laser printing came on the scene first, back in the mid-1980s and ink arrived a little later, during the early 1990s. The aftermarket remanufacturing industry was born in the mid to late 1980s and the innovator and early adopter consumers quickly propelled the aftermarket remanufactured cartridges to a 20% share by the mid-1990s and 30% by the end of the millennium. With a far smaller share of the color market (less than 10%), aggregate aftermarket share has stagnated around 20% ever since!

In order to progress this far, all five stages of the Consumer Adoption Process were satisfied - product awareness, consumer interest, evaluation, trial, and adoption. Furthermore, all these thresholds were crossed during the 1990s despite the products being technically inferior to the OEM versions. With a 30% market share (on monochrome laser) by the year 2000, consumer adoption was deep into the early majority stage and had "crossed the chasm" of consumer acceptance. According to consumer adoption theory, the aftermarket alternatives should have gone on to even broader market acceptance and growth of market share.

Now, at this point, it would be easy to get bogged down in a narrative of ink versus laser, and monochrome versus color printing. We all know the aftermarket has faced many technical challenges within these different categories that may have affected progress along the consumer adoption curve. It's not difficult to argue that the five stages of the consumer adoption process were not satisfied (for example) within the color laser printing sub-category and that the process broke down at stage five as products were rejected because they failed to meet consumer expectations. However, aftermarket monochrome products were adopted despite their technical inferiority so why not color? What else changed that prevented consumer adoption from continuing to develop?

The OEM wake-up call

I doubt the OEM's ever imagined a bunch of entrepreneurs would come up with a means to recover and remanufacture their original cartridges. They were surely confident their government granted monopolies (by way of thousands of patents) would ensure no loss of market share. So, they did what all monopolists do, they exerted their power (in this case over the resellers), charged high prices for the cartridges, and enforced strict terms for continuing to allow them to buy and resell their cartridges.

However, the resellers didn't like being dictated to in this manner so they gave the aftermarket remanufacturers a break by providing a distribution outlet for their cartridges. As a result, consumers became aware of the cheaper alternatives, expressed an interest and quickly adopted the lower priced cartridges, despite their inferior technical performance.

This was the OEM's "wake-up" call that led them to understand the aftermarket represented a serious long-term threat to their business model. The OEM's have always had a go-to-market business dilemma - they have to price the printers low enough for mass adoption and then sell the cartridges at a high enough price to subsidize the losses incurred developing the installed base. If a significant loss of market share on the cartridges takes place, then the business model collapses.

It was these developments that led to the introduction and fine-tuning of numerous blocking tactics to restrict the aftermarket from taking share.

The OEM Blocking Tactics

Rebates:

The first and most effective blocking strategy was the continued deployment and fine-tuning of the rebate model. By introducing sales quotas for their approved distributors and tying their quarterly rebate checks to performance against that quota, the OEM's are effectively able to control market share through the big-box retailers and other Tier-1 distributors and resellers. In leveraging their knowledge that the reseller's sales compensation plans are usually based on the top-line (i.e. $100 OEM cartridges) and that investors and the financial community usually react favorably to top-line growth, they knew they could significantly restrict the impact of aftermarket cartridges. Remember, this has nothing to do with customer acceptance of the aftermarket cartridges, this is the result of powerful OEM's exerting their influence over the resellers in order to restrict consumer access to alternatives.

Think about this one - has the aftermarket share of color been restricted to 8% or so for the last decade because of poor quality products or because of OEM sales quotas and rebate incentives?

Industry Consolidation:

As the big-box retailers, Tier-1 resellers and aftermarket manufacturers have consolidated, it's played directly into the hands of the OEM's and their blocking strategies. It's far easier for the OEM's to exert influence over a smaller number of enterprises than it is a larger, more diverse group of resellers and competitive manufacturers. At first glance, you may think the larger a reseller of OEM products becomes then the more powerful it becomes and, should, therefore, be able to exert more influence over the OEM's. However, this is simply not the case. The resellers all dance to the tune of the OEM's, taking the easy option for top-line sales over profit maximizing alternatives (i.e. aftermarket cartridges).

Control of Distribution:

During 2012-14 HP cut a reported 10,000 resellers off from their products and imposed strict reporting requirements on its remaining authorized distributors, including the requirement to report who they were selling HP brand products to. Imagine having to tell your supplier who your customers are, especially when they're already selling directly to consumers and bypassing distribution in some markets. Now, a manufacturer is entitled to set the terms for resellers of its products so there's nothing inherently wrong with HP from doing what they did, but, let's look under the hood for an underlying strategy behind these tactics.

HP already had all the sales so did it really matter that a lot of the resellers were small businesses and perhaps of little importance to HP? Did they really have a negative impact on HP's image and brand as HP seemed to imply and, as a result not deserve the right to resell HP's products? Or, did HP consider it necessary to weaken these resellers by denying them access to their products, because they represented a potential future threat to their business model? Unlike the Tier-1 retailers and resellers, HP could not control the smaller independents with rebate dollars - someone who sold $50,000 of HP products per year and got maybe two or three thousand back in rebates - it just wasn't enough money for HP to impose a controlling strategy.

Core Recovery:

How to restrict aftermarket share, well just start competing for the cores. The aftermarket setup vast core recovery programs during the 2000s, providing the raw materials for growth so, the leading OEM's simply followed suit. By reducing the number of cores in the supply chain available to the remanufacturers they developed another powerful weapon to restrict development of the aftermarket share.

Engine Diversity:

Never again would the OEM's make the same mistake and allow a single "engine" to develop a large installed base as they did with the original "SX" engine in the late 1980s and early 1990s. Today the life-cycle for hardware is drastically reduced with new models coming out at quicker intervals. It takes time and research and development expense for the aftermarket to develop new products, it takes a time to recover enough cores to place a new product in distribution and to be sure there are sufficient cores to keep it stocked in distribution. There's risk involved for the aftermarket to determine whether a new product announcement from the OEM is going to be successful or not and whether they should devote their efforts to developing an aftermarket alternative. The more new products launched by the OEM's the higher these aftermarket expenses and risks become. Back in the early days and ten products covered 80% of the market, now it takes hundreds of products to cover 80% of the market.

Cartridge Technology:

There's a lot of technology on an ink or laser cartridge these days and you have to ask yourself, is all this necessary or, is it a tactic to thwart the aftermarket from gaining market share? Starting with Seiko Epson on their ink cartridges back in the early 2000s, and continuing at an increasingly rapid pace, has been the placement of encrypted chips on almost every OEM cartridge that comes to market. It's difficult to accept that every feature incorporated into these chips has been developed for the purpose of improving the consumers' experience as opposed to blocking the aftermarket cartridges.

Simply having the ability to plant a firmware update on their hardware that temporarily, or permanently disables aftermarket cartridges, carries far more potential to erode consumer confidence than any conventional brand marketing can achieve.

Legal:

The constant threat of patent infringement, the seeking of ITC General Exclusion Orders to restrict imports, and the bringing of the First-Sale Doctrine into play and placing a heavy cloud over remanufacturers with regard to the responsibility for knowing the core used for remanufacturing was sourced from the United States market after a legitimate "first-sale" in that same market.

Perhaps, by selectively ignoring potentially infringing and potentially counterfeit products sold through channels such as online marketplaces like Amazon and eBay, the OEM's can watch the aftermarket resellers contribute to their own downfall. With the Tier-2 and Tier-3 resellers desperately trying to figure out e-commerce and flooding these marketplaces with low-priced products, what better way for the aftermarket to erode its own reputation for quality, while simultaneously playing directly into the OEM's marketing strategy to discredit lower priced alternatives?

Traditional Marketing:

There's a word out there known as "FUD" - it means fear, uncertainty & doubt and is usually invoked intentionally in order to put a competitor at a disadvantage. OEM FUD campaigns have been aggressively deployed since the aftermarket first appeared on the scene.

Below are links to four FUD campaigns launched by Hewlett-Packard. Take a look and decide for yourself whether these are dragging up memories of toner bombs and other quality issues from twenty years ago or whether they legitimately apply to the products available from the top tier aftermarket manufacturers and remanufacturers that exist today.

As you're thinking about whether these FUD campaign videos apply to today's market or not, think also about the fact that the OEM's already sell the very aftermarket products they denigrate in their marketing collateral. They have to, in order to support their MPS programs.

They sell managed print service contracts to their largest, their very best, premium customers who may have thousands of printers deployed throughout their organizations. These printer fleets are always made up of a variety of OEM hardware - i.e. there may be HP, Lexmark, Oki, Kyocera Mita, devices etc. When any of these OEMs prepare a multi-year managed print services contract who do they turn to for cartridges to fit on these devices? Well, you can be sure it's not their OEM competitors. HP is not going to Lexmark, and Lexmark is not going to HP, for cartridges to fit into the devices they need to service so, they go to Clover or LMI Solutions and source aftermarket cartridges - the same cartridges they would prefer to have everyone believe are technically inferior and unsuitable for consumers to use!

This is the ultimate hypocrisy in terms of "do as I say, not as I do!"

Logistics & Customer Service:

The OEM's, the big-box retailers, the Tier-1 resellers and distributors, the Tier-1 aftermarket remanufacturers, all have done a great job in terms of logistics and customer service. All have invested heavily in information technology to ensure they have the ability to deliver quickly, reliably and cost-effectively. All have invested in state-of-the-art customer response systems (CRM) to ensure they can quickly and efficiently pull up customer history and records for purchasing patterns and problem resolution. The Tier-2 and Tier-3 resellers have allowed their larger competitors to get ahead in this crucial aspect of modern day business and, of course, it has now become part of the overall blocking strategy.

Blocking Tactics - Conclusions:

It's difficult not to be impressed with this long list of defensive strategies that have been deployed by the OEM's. For sure, they are tough, intelligent competitors. They know their competition and they know how to neutralize the market players in order to achieve their goals. In fact, the OEM blocking strategies and communications have been so effective that I think even the resellers of aftermarket products have come to believe its negative messaging!

The thing is, this blog is about the consumer adoption curve and product life cycles but, so far, I've only spent a little time specifically on this topic. However, the reason for this is that the aftermarket ink and toner cartridges have already been through the first stages of the adoption curve, successfully reaching the "early majority" stage and even "crossing the chasm" toward greater adoption. Consumer interest and adoption is not the issue here, it's the story of how and why, despite the consumer interest, the path to a greater share of the overall market has been blocked.

The importance of the fact that consumers have already demonstrated a willingness to adopt the aftermarket value proposition must not be underestimated. Knowing this is a huge advantage for independent resellers who want to restart their business development. The challenge is not whether customers want the products, it's figuring out effective ways to circumvent the OEM roadblocks and to start to increase market share.

What next?

Well, it's time for the aftermarket to fight back.

To schedule a no-obligation consultation with us to learn more about our turnkey digital business transformation service for office products resellers please click on the link below.

The quality of the aftermarket product proposition today compared to when it passed those first critical consumer acceptance thresholds back in the 1990s is simply night and day. However, with the big, powerful retailers and resellers firmly in the pocket of the OEM's, there's been no effective path to get the aftermarket message to consumers and to educate them on the value proposition and the availability of these quality alternatives. Remember, this was not the case when the resellers in the 1990s gave the aftermarket industry a break, putting their products into the distribution channels and allowing consumers to become aware and to adopt them.

In the next blog in this series, I'll be presenting my view on where the battlegrounds will be, and what tactics may be utilized in the fight for market share. The success of many of the OEM blocking tactics is dependent on the existing cartel arrangement, (big-box retailers, Tier-1 resellers and distributors, and the Tier-1 aftermarket manufacturers), being preserved. Sure, it's possible one of the big guy's could break ranks and influence change but, I think that's unlikely.

My focus will be on the Tier-2 and Tier-3 resellers and distributors, with whom the OEM's have little to no influence over how they conduct business. In conjunction with the newly emerging Chinese superpower manufacturers of high-quality new-build compatibles - now, that's a new partnership which has the potential to carry on where those early pioneers of the aftermarket for ink and toner started out.

In the meantime, why not check out our free eBook with a comprehensive assessment of the office products industry and the opportunities to develop significant sales growth in a challenging environment despite the ongoing consolidation of a mature industry.